{kind=link}

Buy Now, Pay Later: Should Your Business Use BNPL Platforms? (With Examples)

At first glance, BNPL platforms seem too good to be true. “Will I have to pay double in interest? Is this a pyramid scheme? What’s in it for them?” If you buy into them now, will you pay the price later?

BNPL platforms have become a tried and true part of the ecommerce experience. These platforms have seamlessly integrated into online shopping experiences. More than 50% of U.S. customers have used BNPL platforms in the past year. You could argue that lacking a BNPL platform can hinder some businesses, whereas some would've thought the opposite in the past.

But are BNPL platforms right for just about any business? Are there risks involved? And are the benefits convincing enough to go all in?

In this article, you will learn:

- What Is BNPL (Buy Now, Pay Later)

- How BNPL platforms work

- The benefits of BNPL platforms for your ecommerce business

- The risks involved with BNPL platforms

- 3 Popular BNPL Platform Examples

Let’s get into it.

Need expert help selecting the right tool?

With one-on-one help, we guide you to your top software options. Narrow down your software search & make a confident choice.

What Is BNPL (Buy Now, Pay Later)?

A Buy Now, Pay Later payment platform is a short-term payment plan that lets your customers make purchases and pay for them later. These platforms are also usually interest-free. BNPL payment methods give customers the freedom to immediately (or impulsively, perhaps) make their purchases and pay them back in set payments over time.

Think of a customer making a $200 ecommerce purchase. Instead of paying up in one go, they can pay for their item in four interest-free payments of $50.

As a customer, it’s pretty easy to use BNPL platforms. But what if you’re the business that’s using them? Turns out it’s still pretty straightforward. The business receives the full payment of the item immediately, minus any fees—similar to credit card payments. You don't have to manage much financing more than that.

Buy Now, Pay Later service providers take on the hard stuff. You get to focus on growing your business instead of worrying about insurance policies, collecting payments, or any of that jazz.

How Do BNPL Platforms Work?

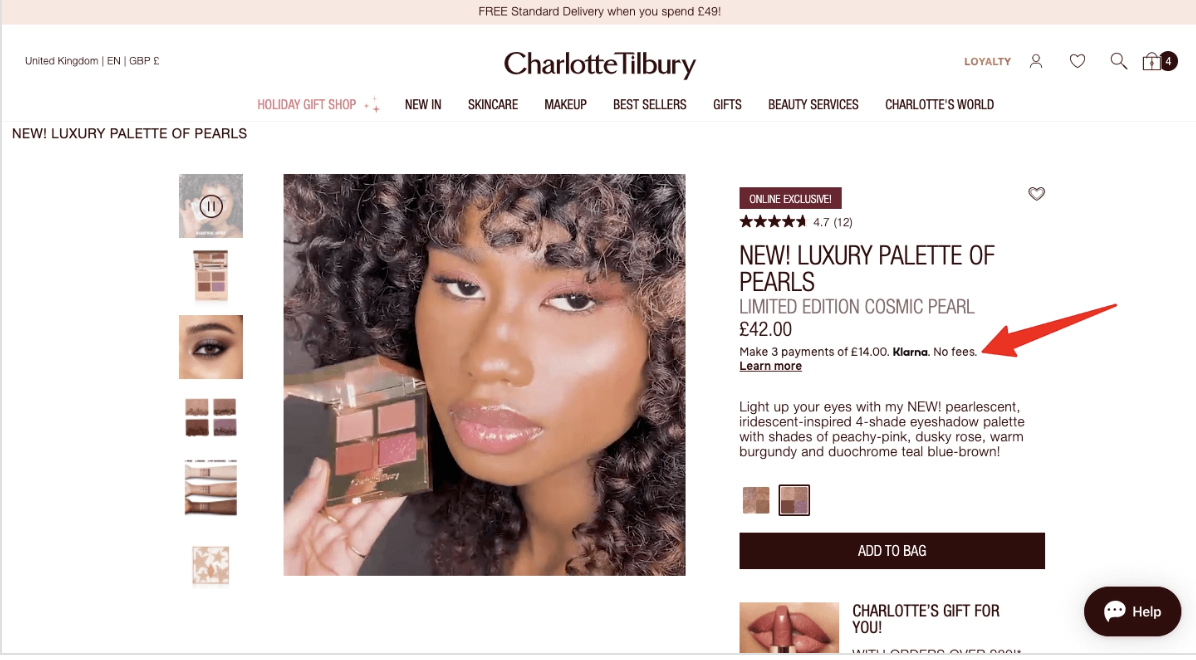

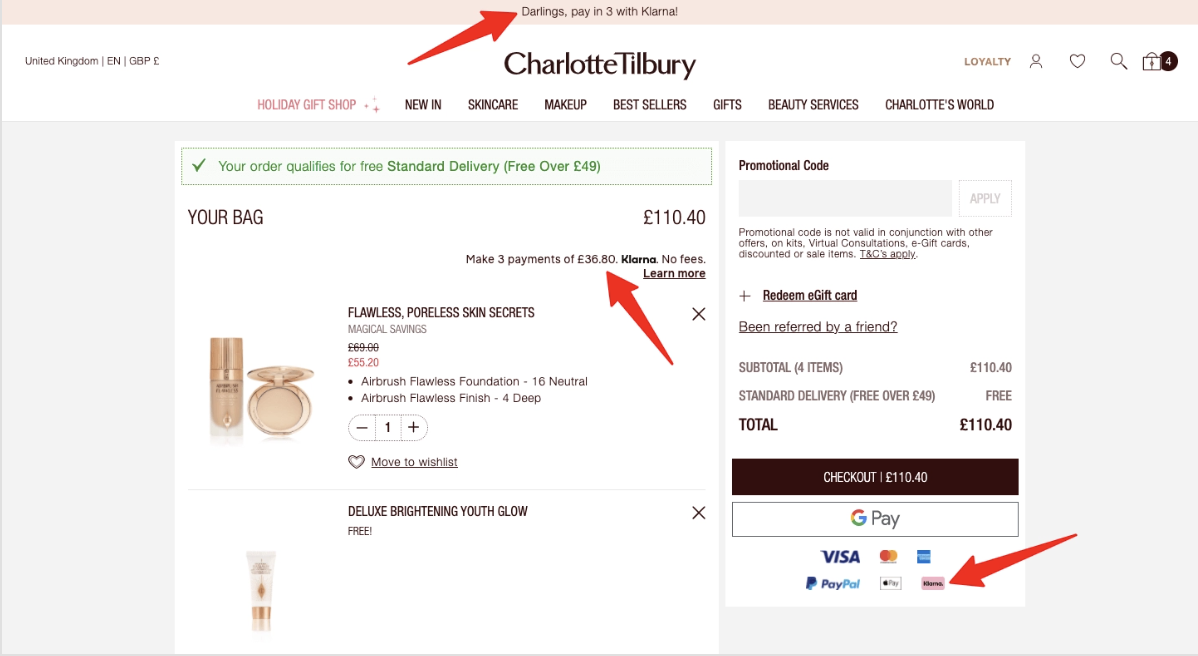

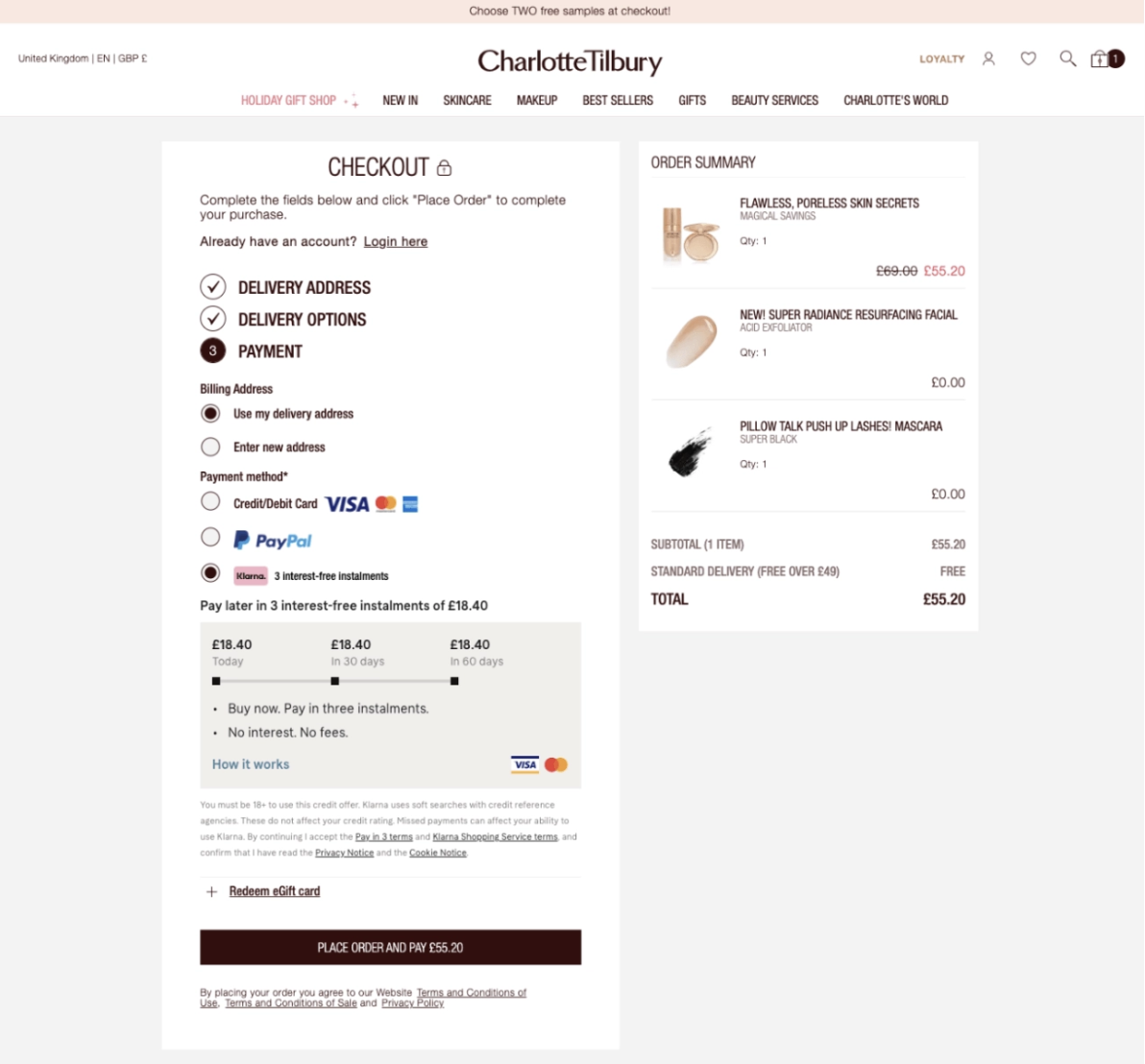

Not all BNPL platforms are created equal. While a platform like Afterpay focuses only on four-step installments, Klarna gives you room for six-month payment plans and has a pay-in-30 method, where you can return what you don't want and pay only for what you keep in a 30-day window.

But even though there are minor differences between different platforms, some things apply to all Buy Now, Pay Later services. You can find them as an option in the payment flow, right next to credit cards, PayPal, and other payment methods. You can pay via a check or bank transfer; payments can also be automatically deducted from your debit card, bank account, or credit card.

How do these things work anyway? It’s usually a few simple steps to follow:

- A customer makes a one-time purchase on an ecommerce website. At checkout, they go for the Buy Now, Pay Later option in the payment form.

- The customer is directed to the Buy Now, Pay Later platform website or app to create an account or log in.

- Then, they can accept the repayment terms, which vary from bi-weekly to monthly, depending on the platform.

- Once the customer is approved, they make a downpayment towards their purchase. They should know if they’re eligible for BNPL platforms within seconds of attempting their purchase.

- Then, the customer can start paying off the rest of their payment amount in interest-free installments.

Although BNPL arrangements often don't charge interest, they have a fixed repayment schedule ranging from several weeks to months. Customers know what they’ll need to pay each time, and the repayment is usually divided into similar payments. Just think of it as any other sort of consumer loan.

What Are the Benefits of BNPL Platforms for Your Ecommerce Business?

With the ecommerce boom since 2020, Buy Now, Pay Later services quickly picked up traction. And they don’t seem to be losing steam anytime soon, either.

Having a BNPL platform attached to your ecommerce experience is an easy way to pull in customers. Let’s take a look at the benefits.

1. Convenience for your customers

With BNPL platforms, you’re giving customers a seamless and customized payment journey on a silver platter. In 2023, when attention spans are shorter than ever, a frictionless checkout experience can be your winning ticket. Not to mention, you’d be giving your customers the flexibility and freedom to choose how they want to pay.

2. Reaching more customers

Newsflash: Gen Z is adopting the Buy Now, Pay Later mindset. Yup, it’s a lifestyle at this point. And one without even needing a credit card. 26% of millennials and almost 11% of Gen-Z shoppers used Buy Now, Pay Later platforms for their recent online purchases. BNPL platforms also have their own brands and marketing endeavors (look at how beautifully Stripe does it), which can only mean good things for your business as you gain another way to reach new customers.

3. Increasing your conversions

Numbers don’t lie. According to a new report, having a BNPL platform for your customers increases ecommerce conversion rates by 20-30%. Shopping demographics across the board are embracing this payment method so much that Buy Now, Pay Later sales are expected to double by 2024 (and that’s just around the corner!)

4. Boosting your average order value

BNPL platforms are great low-barrier ways for customers to invest in larger purchases more comfortably. They can ease into bigger purchasing decisions by breaking up their payments into smaller installments that work for them. This only means good things for your business and your average order value, whether you sell higher or lower-priced goods.

If you’re in the business of higher priced goods, you attract customers more easily with Buy Now, Pay Later platforms. If you sell lower-priced goods, you increase your odds of customers making multiple purchases of your products or services. It’s a win-win.

Are There Risks Associated With BNPL Platforms?

Clearly, there are upsides to having BNPL services working for you. But are there any risks on the horizon? Or is it just your classic fear-of-technology-advancing talking? Let’s take a closer look.

1. Risk of fraud

Although most BNPL platforms work to be secure, certain risks come with a customer sharing personal information with a BNPL platform. One of these risks is giving customer data to a third-party provider unknowingly. Businesses that adopt BNPL platforms can end up sacrificing their customer’s privacy.

Customer data can be used to monitor behaviors that can increase profitability. This lack of transparency creates risk for the consumer and can lead to losing customer loyalty for your business. To protect your customers and your business, we recommend looking into fraud prevention solutions, like doing a manual review of your security standards and installing fraud prevention software.

2. Hidden charges and deferred interest

The main appeal of Buy Now, Pay Later services is that you can loan something without paying interest. But there could be a catch. Some BNPL platforms have a “deferred interest plan,” meaning that paying interest is only deferred for a preliminary period.

Suppose a customer doesn’t manage to pay off their installment in that preliminary period. In that case, they can be charged interest on the total purchase amount—not just on the down payment installment.

For context, if you paid $100 for a product with a deferred interest plan, you'd be charged interest on the total of $100. It wouldn’t matter how much you had paid down in advance. Talk about wallet stress!

Luckily, these terms and conditions should be easy to spot if you take the time to read the agreements BNPL platforms provide you. Language like "no interest if paid in full within six months” indicates the risk of deferred interest charges.

3. Fewer regulations and less protection for customers

Buy Now, Pay Later services have had a quick rise to fame, so it makes sense that there are fewer regulations surrounding them. However, this also means that customers have fewer protections to lean on when things go wrong.

Businesses using BNPL platforms can only do so much to help alleviate this. This makes it hard to settle disputes or return products bought with the BNPL method. Sometimes a credit card just feels easier.

3 Popular BNPL Platform Examples

We’ve learned so much about BNPL platforms, how they work, and their risks and benefits. But what are some real-life examples out there right now? Let’s get into a few that have caught our eye in the past few years.

Affirm

Affirm’s low-stakes bi-weekly interest-free payments make them a great choice for everyday purchases. They also have revenue accelerator features that are great for businesses that choose to adopt their platform.

Adaptive Checkout, one of their features for businesses, offers flexible and relevant payment options in one view for a seamless customer experience.

Afterpay

Unlike most four-week repayment setups, Afterpay allows up to over six weeks—with no fees when paid on time. The Afterpay app has features like fraud detection, data security, and payment fraud detection. They cater equally to shoppers and business owners with different features to offer.

Klarna

With easy purchase management and promotional messaging, Klarna helps businesses create a smooth shopping experience all the way through. They also refer shoppers to their partners via integrated marketing campaigns and their shopping app. Not to mention, they have features in place that make settlements and returns easy to manage.

Need expert help selecting the right eCommerce Solutions Software?

If you’re struggling to choose the right software, let us help you. Just share your needs in the form below and you’ll get free access to our dedicated software advisors who match and connect you with the best vendors for your needs.

Are You Buying Into The BNPL Hype?

Buy Now, Pay Later platforms have made their way into the ecommerce zeitgeist over the past few years. With Apple entering the BNPL fray with Apple Pay Later, you can expect BNPL to continue growing in popularity.

As we've explored, every new payment gateway solution involves risks and benefits. What do you think? Are they worth buying into, or are you sticking to classic credit card payment setups? Comment below with your thoughts.

For more on the latest insights, tools, and tips for ecommerce, sign up for The Ecomm Manager newsletter today!

You might also like: